Is your ISMS leadership exposed by weak documented information controls?

When an audit comes for your ISO 27001:2022 certification, the spotlight never lands on your confidence—it lands on your documented information. Clause 7.5 is not filler. It’s the test of whether your security claim is real or just a storey you hope everyone believes. In boardrooms, at regulator tables, and with every major client, leadership is measured by controlled evidence—not just an action plan, but the receipts.

The backbone of trust isn’t flashy controls—it’s brutal documentation discipline when the heat arrives.

Too many strong teams stumble. Your systems might crackle with security tech, but if documentation is outdated, scattered, or hiding in six months’ worth of email, you are gambling with more than just compliance. You’re betting your reputation and competitive edge on hope.

The real price of weak documentation

Clause 7.5 is not a boring records requirement—it is the nerve centre for any business claiming leadership in information security. The board expects answers in seconds. Regulators want to see proof, not promises. When your documents are meticulous, versioned, and alive in your ISMS, you lead. When they’re lost, your authority unravels. Earning audit trust starts the moment you treat documentation as the heartbeat of your company’s defence.

Most audit failures don’t start with technical gaps. They begin with documents that can’t be found—or worse, can’t be trusted.

Book a demoWhat, exactly, does Clause 7.5 mean for your ISMS proof—and how do auditors catch you out?

ISO 27001 Clause 7.5 zeroes in on the unsexy reality: documentation isn’t “nice-to-have.” It’s the wall between “we tried” and “we delivered.” Compliance teams that treat documentation as a formality—the ones who slap together templates or file records as afterthought—are first to get flagged by an auditor. What works? Records curated for your actual risks, your sector, your controls—not “ISO by the book,” but auditable proof that you own every control and can show it when asked.

The critical artefacts your ISMS cannot fake

Trying to pass an audit without these is asking to fail:

- ISMS scope statement: — it’s your “what we protect” in black and white (Clause 4.3)

- Security policies and objectives: — evidence you set the rules and live by them (Clauses 5.2, 6.2)

- Competence, awareness, and training logs: — audit-proof that you don’t just train once and forget (Clauses 7.2, 7.3)

- SoA (Statement of Applicability): — the “what and why” for every control in your ISMS (Clause 6.1.3)

- Risk assessment and treatment logs: — live evidence you know your threats and respond (Clauses 6.1.2, 6.1.3)

- Evidence of operational controls and monitoring: — do you test, track, and fix for real? (Clauses 8, 9)

- Records of improvement actions and reviews: — proof that you close the loop, not just talk about it (Clause 10)

Every one must be alive, signed off, and instantly retrievable. Auditors won’t chase intent—they hunt for concrete, up-to-date proof. Miss these, and you lose not just the audit, but your stakeholder’s confidence.

Audit pain starts with ‘almost ready’ paperwork and ends with real consequences.

Make documentation the reflection of your actual risk—not a checkbox

Templates are a graveyard for compliance reputation. Your real-world risks—supplier lapses, process errors, contract misses—demand living artefacts: supplier diligence logs, true incident records, key decision minutes. If it matters in a board update or to a regulator, it should be documented under the ISMS and ready on demand. Get this right and you trade anxiety for instant credibility.

ISO 27001 made easy

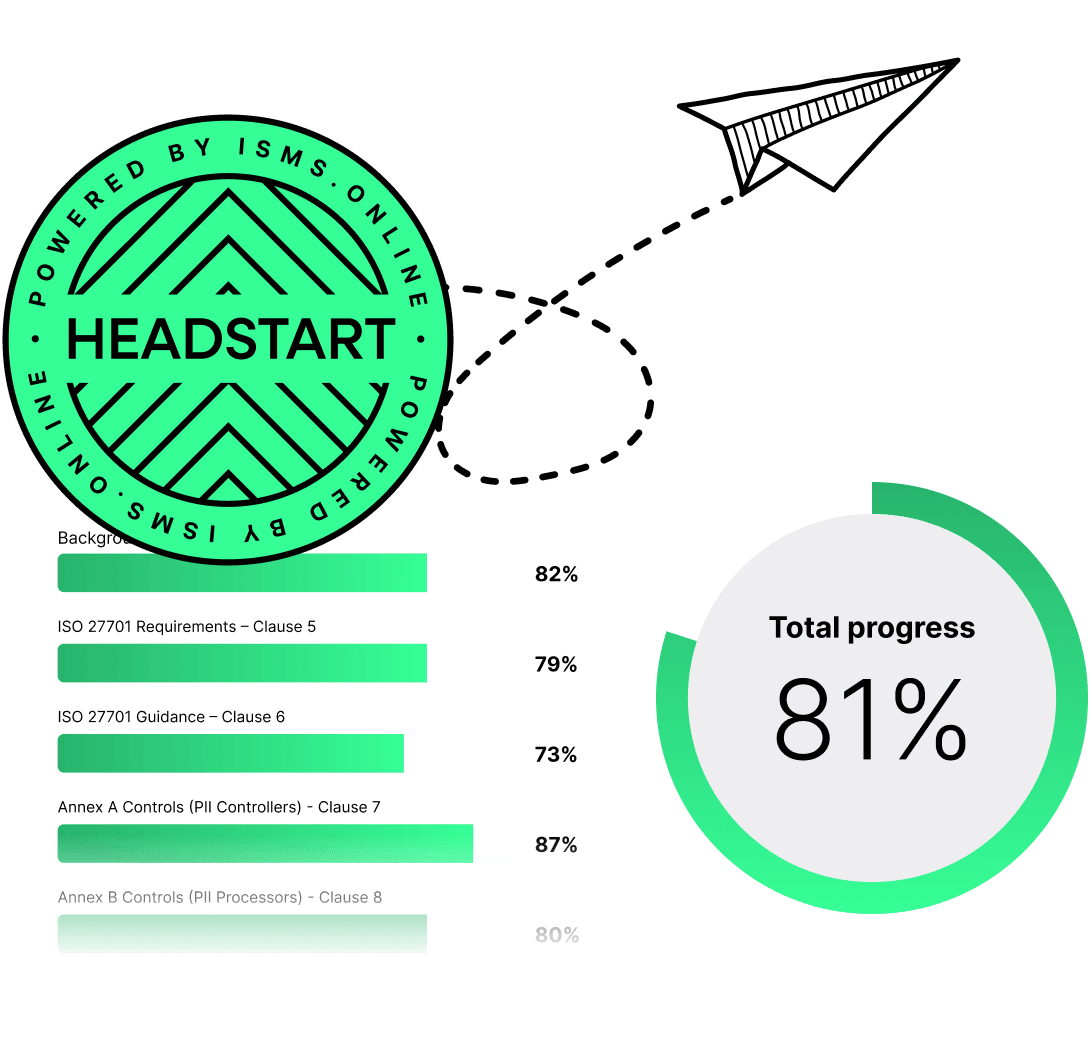

An 81% Headstart from day one

We’ve done the hard work for you, giving you an 81% Headstart from the moment you log on. All you have to do is fill in the blanks.

How do you build ISMS documentation that’s controlled, reliable, and truly audit-proof?

You win by acting like a control freak—down to the smallest file. ISO 27001:2022 Clause 7.5 isn’t vague; it outlines a lifecycle for every artefact: from creation and ownership, to version, access, review, right through to controlled destruction.

-

Ownership and Traceability

Every document lives or dies by clear ownership—who’s responsible, when was it last reviewed, and how is it tracked? Anything less is a recipe for audit pain. -

Standardisation and Centralization

Your files aren’t weapons if they’re spread across inboxes, personal drives, or outdated SharePoint folders. One platform, one structure, total control. -

Ruthless Review and Approval

Ad hoc reminders are not a system. Reviews must be scheduled, tracked, and mapped to controls. Audit-ready means “show me the sign-off,” always. -

Access Control with Real-Time Logs

Editing rights are sacred. Only assigned owners or approved delegates touch the record. Everyone else is a witness, not an editor. -

Version and Change History

Static files age; living logs make rollback, comparison, and evidence a non-event. Change who, when, and why—locked every time. -

Retention and End-of-Life

Forgetting an outdated document is just waiting for a regulator to find it. Automate retention, schedule deletion, and prove you wiped every liability away.

| Lifecycle Step | Major Audit Failure If Missing | What Auditors Expect |

|---|---|---|

| Ownership | No accountability, “lost” files | Named owner, tracked review dates |

| Central Formatting | Chaos, retrieval mess | Unified, digital records |

| Review/Approval | Version confusion, missed updates | Authorised sign-off, full audit trail |

| Access Control | Unauthorised edit or leak | Real-time permission and log evidence |

| Version Control | Gap in evidence, rollback impossible | Tracked changes, history, instant proof |

| Retention | Stale risks, accidental use | Timed deletion and audit-ready logs |

One shadow document—or lost approval—creates audit chaos no technology can mask.

Discipline here is the difference between a reputation for excellence and an ISMS that unravels when it counts.

What separates “show-ready” from “scrambled” when the auditor appears?

Audit days are stress tests for leadership, not just process. Winning teams don’t sweat evidence—they have it baked in. Losing teams? They scramble, plead, or guess when asked for proof.

Here’s what makes or breaks audit resilience:

- A unified artefact register: that acts as your single source of ISMS truth.

- Instant, logged retrieval: showing the who, what, when, and why of every critical action.

- Full version history, live backups, and secure rollback: —no “finalV2” shortcuts.

- Role-based, real-time access audits: defending every edit.

- Demonstrable proof: every record is readable, maintained, and eliminated at lifecycle end.

- Mapped retention policies: aligned with legal and regulatory duty.

Audit surprises don’t exist when your ISMS runs on operational truth, not last-minute hustle.

ISMS.online makes this your default. No “scramble mode,” no guessing. Just solid, real-world evidence served up, day or night, for any stakeholder who needs to believe you.

Free yourself from a mountain of spreadsheets

Embed, expand and scale your compliance, without the mess. IO gives you the resilience and confidence to grow securely.

Where do top teams fail—and how do leaders convert gaps to reputational strength?

The harsh truth? Most ISMS breakdowns and audit failures aren’t caused by clever threats, but by small cracks: abandoned handover emails, outdated reviews, orphan artefacts drifting outside the system, or permissions that rot over time. These silent failures don’t impress auditors—or the board.

Silent risk signals include:

- Legacy versions left exposed to everyday users

- Missing proof of review or sign-off after urgent updates

- Rogue copies downloaded outside monitored channels

- Logs quietly over-staying retention, or quietly lost

- Vague ownership in high-stakes scenarios

Documentation isn’t a memo to survive audits; it’s an asset that builds trust you can’t buy with software.

Leaders who win:

- Centralise everything within an ISMS built for evidence, never just documentation.

- Automate permissions, reviews, alerts, and versioning, closing every manual back door.

- Assign and enforce artefact ownership—no document left drifting.

- Rehearse audits so proof is muscle memory, not post-hoc panic.

- Make security a culture, not a compliance fire-drill.

How does disciplined documented information control drive real-world reputation?

An ISMS is only as strong as its evidence. Boards, regulators, customers—they all judge your credibility on the speed and confidence of your proof. When policies, approvals, corrections, and decisions flow through a single, trusted channel, you win more than audits. You command reputational strength.

The leaders who own documentation, own the narrative, and set the market’s trust agenda.

ISMS.online customers create reputational advantage with living, trustworthy documentation at the core. Artefacts are not paperwork—they are provable, current, assignment-tracked, and always stakeholder-ready.

Manage all your compliance, all in one place

ISMS.online supports over 100 standards and regulations, giving you a single platform for all your compliance needs.

Could your team satisfy every ISMS evidence request—without hesitation—today?

In a real audit or a board “show me,” there’s no time for search or guesswork. If you can’t produce the right artefact, mapped, reviewed, and logged in seconds, your ISMS is a liability, not a shield.

Audit-reliable maturity is a move from “it’s somewhere” to “it’s here—proof attached.” Only then can you guarantee regulator calm, board confidence, and customer trust in every crisis.

If your leadership can’t prove it, you can’t defend it; the standard is instant, not ‘eventually.’

Command your ISO 27001 documented information. Lead with ISMS.online.

Risking your audit—and reputation—on outdated, uncontrolled, or scattered files is a choice. Choosing ISMS.online is refusing to let documentation become your weakest link. Every artefact, every version, every approval locked, automated, and always at your fingertips.

You’re not aiming to scrape by another audit. You’re taking ownership of your ISMS’s living foundation—documented information that leads, commands, and earns trust every time. Make that move today.

Frequently Asked Questions

What new risks come with manual documented information management in your ISMS?

Manual handling of ISMS documentation—think scattered spreadsheets and email trails—invites costly, avoidable trouble. Each handoff multiplies the chance for lost updates, missing evidence, or outdated policies slipping through. When proof of compliance is needed on demand, your team faces a scramble that reveals weaknesses rather than resilience. Automated platforms, by comparison, track every change, flag missing sign-off, and put ironclad audit trails within reach, turning routine compliance into a business advantage instead of an anxious firefight.

How do manual methods undermine audit-readiness and trust?

- Missed deadlines or approvals vanish in crowded inboxes.

- Version confusion makes it impossible to prove what really happened.

- Gaps in access logs weaken case for system integrity.

- Repeatedly chasing colleagues drags down performance and morale.

When documentation is automatic, your audit game shifts from catch-up to confident demonstration. Trust rises on both sides of the table—and that peace of mind lasts far beyond audit week.

How can you build direct links between ISMS controls and supporting documented information under Clause 7.5?

Clause 7.5 demands every ISMS control—policy, procedure, or technical measure—is buttressed by documented evidence of compliance. The gold standard is a living register that pairs each control with its relevant documents and evidence, updated in real time. This isn’t just for auditors; it streamlines internal reviews, speeds up onboarding, and demystifies compliance for business leaders. When every file, approval, and status change is visibly mapped, you gain control and clarity—no more guesswork come audit season.

What does best-in-class mapping really look like?

- Each ISO control is mapped to both authoritative documentation (“this is how we do it”) and proof records (“here’s where we did”).

- Owners, review cycles, and update dates are all woven into the register for instant traceability.

- When business changes trigger new risks, linked documentation and evidence automatically prompt review or updates.

ISMS.online activates this mapping with visual dashboards and automated notifications, making your compliance landscape both visible and defensible.

Why is distinct ownership of ISMS documentation a game-changer for compliance leaders?

Clear ownership is the difference between a living ISMS and an illusion of control. If every policy, checklist, and evidence log is assigned to someone by name, accountability becomes real, not just implied. Ownership ensures deadlines are tracked, updates don’t stall, and urgent tasks don’t languish in a vacuum. The ripple effect is culture-shaping: teams see compliance not as punishment, but as opportunity—to stand out for reliability, trust, and performance. Without ownership, it’s all too easy for critical items to slip through when pressure mounts.

When responsibility’s diluted, nobody feels the hit—until everyone does.

How does ISMS.online embed this ownership across your team?

Automated task assignment, reminder cycles, and visible approval chains hold every stakeholder to account. Owning a document means owning its reputation; ISMS.online ensures your leadership footprint is unmistakable.

What’s the bigger message your documentation habits send to auditors and the board?

Every touchpoint with your documentation tells a silent storey. Scrappy file structures, unsigned records, or out-of-date policies hint at a risk-blind culture—giving auditors reason to probe deeper and leaving the board uneasy. In contrast, up-to-date, versioned, and instantly retrievable records shout rigour and care. These subtle signals make or break first impressions during reviews. Your ISMS becomes more than a checklist: it’s a living reflection of your company’s operational maturity and leadership priorities.

Trust is front-loaded or lost early. Teams that prepare, win confidence before they even speak.

What habits signal you’re ahead of the curve?

- Review dates aligned with actual business shifts—not just annual reminders.

- Fast, organised access proves “audit-ready” isn’t just a claim.

- Internal spot-checks and peer reviews surface issues before outsiders ever glimpse them.

When ISMS.online structures these workflows, your leadership shines through each document retrieved.

How does a platform like ISMS.online future-proof your documented information as standards and the business change?

Regulatory swings and internal pivots are the only constants, so your ISMS needs to evolve faster than risk does. ISMS.online moves with your business: new ISO controls, revised ownership, added templates, or changed team roles all ripple instantly across your documentation. As requirements grow more complex, automation ensures that compliance isn’t just maintained—it gets sharper with each cycle. Your team adapts seamlessly to new demands, keeping you several steps ahead of emerging threats and giving your board fewer sleepless nights.

What platform features make adaptation effortless?

- One-click policy updates that cascade changes across linked evidence logs.

- Automated evidence gathering as new controls or risks appear.

- Flexible permission and audit structures ready-made for mergers, reorganisations, or regulatory overhaul.

Investing in ISMS.online means your compliance never freezes in time; it evolves on auto-pilot, putting you at the leading edge.

What leadership edge does bulletproof documentation provide for compliance professionals?

Excellence in ISMS documentation separates you from the cautious majority. When every policy and evidence trail is at your command, your standing with leadership and peers transforms—you move from box-checking to benchmark-setting. You’re now the first call in a crisis, the loudest voice in board conversations, and the north star for compliance credibility in your sector. Automated documentation with ISMS.online arms you with immediate confidence and proof, even as others scramble at audit time. This authority builds not just safety, but a brand of trust your competition dreams about earning.

Documented mastery reshapes what others see as compliance—making trust your signature and crisis management your stage.

How can you activate this status?

Make ISMS.online your operational home base and tie every compliance artefact to your team’s identity. When you treat compliance as a leadership discipline, every stakeholder meeting becomes a showcase for your expertise—and every audit, a stage for your team’s confidence.